When Fely and I were both employed, the company we worked with really provided very well for our healthcare. However, when the company opted to give us early retirement, our healthcare also ceased. Thus, it gave us a very big lesson that we must make sure that while we are working and the company provides for our short term healthcare, we must invest on our own long term healthcare too. We do not want to experience the stories of Jose and Juan and many others who have struggled and still is struggling financially because of a medical crisis in their life.

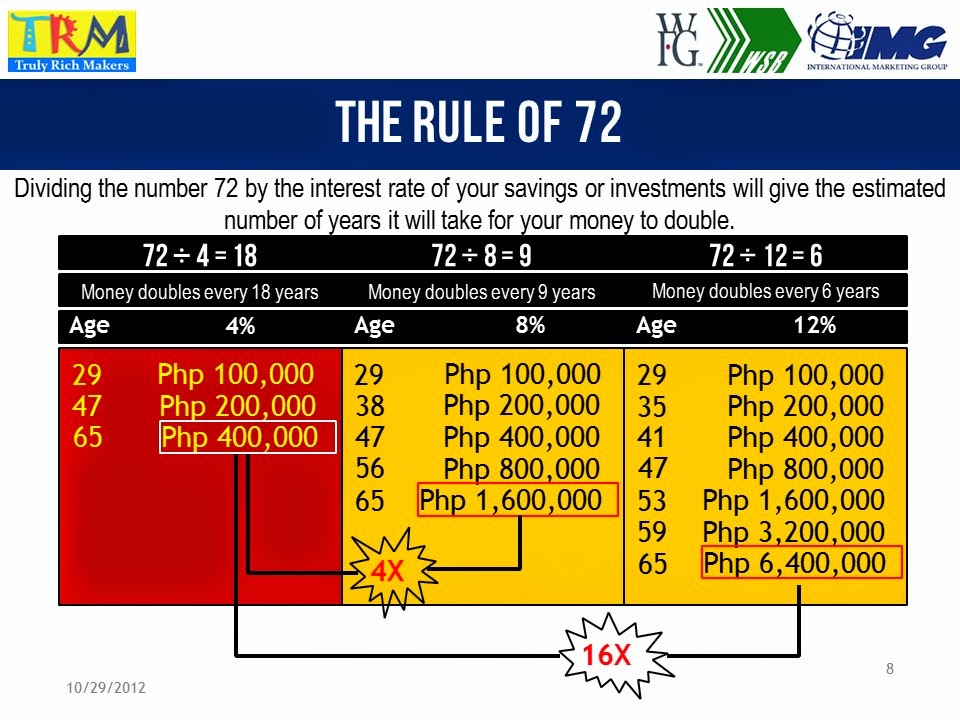

So this is the first investment that we took care. We acted on it. We got ourselves and our children, long term healthcare. Our entire family are secured that any medical crisis we might encounter, we have money that we can use. Fely and I do not need to sell off properties; we do not have to incur debts. We have a solid financial foundation. We calculated how much we would need in case of a medical crisis, as well as for the basic medical needs. By basic, this includes maintenance medicines, and vitamins, and supplements. We calculated the future value of what we spend today to the year we project we actually will need it. We used an inflation rate of 7%.

I had seen many families that went bankrupt because of a medical crisis. One of them is June; a retiree from a prestigious local company. In his retirement years, he had cancer. All their lifetime savings and properties were wiped out in just a matter of months. He even had to ask financial support from family and friends. He had to even resort to borrowing money. Finally he succumbed to the disease not because there is no cure but because he has exhausted all his resources and his family could no longer support him. He died penniless and in debt.

Jose a seafarer, with very high pay had lots of money. Whenever he arrives from months of sailing as captain of a chemical tanker, the whole “barangay” celebrates days of feasting and drinking for his many friends. He lived a life of a multi-millionaire. But one day, he was diagnosed with heart ailment. For the first year, his company and his savings enabled him to survive.

However, his resources to pay off for his medical needs and daily expenses did not last long. Worst, since he no longer can ably steer the ship, he was retired by his company. Since he is retired, he no longer is covered by the healthcare the company previously provided him. Even if he is still is below 60. Because of his heart condition, he is not taken in even on a lower post. Thus, he no longer had income, and along with that, his drinking buddies abandoned him. Worst, his wife left him alone. Now, on his late 50's, he is lonely, penniless, jobless, and cannot afford to care for his health.

Another guy we met was Juan, a very young Training Manager of one of the fast-food chain in the Philippines. Even before he reached 30, he had a stroke rendering half of his body paralysed. Like the experience of Jose, the company only took care of him on a very limited number of months. Eventually he was also asked to resign. So the short term health care he enjoyed as employee is no longer in effect. Since he did not invest on his own short and long term healthcare, he had to pay for his physical rehabilitation from his own savings, and from the help of his family. This definitely put a terrible stress in the family's finances.

Peter is another example of those who had very successful career in the past, had high position, and well covered short term health care. He is almost always on travel and had assignments overseas as a Manager in a Semiconductor Manufacturing. However, he had contracted kidney problem that necessitated medical attention.

Initially, he was covered by the company he worked with. But, of course as usually what happens, the company would only cover medical needs of an employee on a limited basis. This left him to fend for his own needs. Since he did not invest on his long term healthcare while he was gainfully employed, he did not have any back up plan. In his early 50's, he is unemployed and survives by the income of his small business, and by asking help from his former co- employees and friends for his regular Dialysis that already had cost him millions. After 4 years, he eventually died leaving the family with a mountain of debt.

We met many June, Jose, Juan and Peter of different ages, who went through the pain and difficulties in their finances due to medical crisis. People really go bankrupt if they do not have the basic short term and long-term healthcare. It does not matter whether you are in the early part of your career or in the last quarter of your work life. The lesson we learned from these people we met is clear, we have to make sure that in building our solid financial foundation, we must indeed start it by securing our own long term health care. And if we do not have a short term healthcare, we must secure it too!

We have completed our 5 year investment on this Long term healthcare. With just the interest earnings of our long term healthcare coverage, we can sustain our daily basic maintenance or even a medical crisis, which we pray won’t happen. But just in case it does, we have more than a million pesos to cover for that. We won’t have to sell any property nor borrow money. Better yet, we expect and claim that we will be healthy, and thus, would use the interest of this invested money to help other people like Juan, Peter, and Jose who are in desperate need. After completing our Kaiser HealthBuilder Premium , we took another Plan. A bigger plan which is a

7-Year Kaiser Ultimate HealthBuilder!

We do what we preach!